.png?width=3157&height=1832&name=PZF%20logo%202023%20FINAL_Light%20(3).png)

Ivan Ferrari , Head of Business Development, Elevandi

One of the hot topics debated in finance recently is the concept of “Tokenised Deposits.”

It is an intriguing idea. The core concept is simple: they are a type of financial asset that represent traditional bank deposits, such as savings or checking accounts, that have been converted into digital tokens. These tokens are typically created on a blockchain, which allows for the immediate and easy transfer of ownership and the tracking of transactions in a secure and transparent manner.

How can we look at our present payment system through this innovation?

Today’s piece explores the concept of Tokenised Deposits and its connection to the banking ecosystem. My hope is that it will offer a fresh perspective through which to view FinTech’s never-ending innovations.

In short:

What are the benefits of tokenised deposits? How do they work? How do they differ from stablecoins? Why would banks consider implementing them? We’ll explore all of these questions in today’s piece below.

Summary:

- What are Tokenised Deposits and how different are they from Stablecoins?

- Actionable Insights

- An Intro to Tokenised Deposits

- An intro to Stablecoins, Tokenised Deposits’ competitors

- How are tokenised deposits different? A deeper dive

- BIS’ View on Tokenised Deposits

- The Oliver Wyman report on Tokenized Deposits

- The Point Zero Forum Roundtable “Who will Emerge the Digital Money Winner: Stablecoins or Tokenised Deposits?”

What are Tokenised Deposits and how different are they from Stablecoins?

Image created by BING AI

Actionable Insights

If you only have a few minutes to spare, here’s what you should know about “Tokenised Deposits.”

- What are Tokenised Deposits? Savings or checking accounts, that have been converted into digital on-chain tokens.

- The benefits of Tokenised Deposits: While being a relatively new development in the financial industry, Tokenised Deposits have the potential to revolutionise traditional banking by providing greater flexibility, increased liquidity, lower transaction costs, increased accessibility, fast finality, programmability, and transparency.

- Still under fractional reserve. Tokenised Deposits are still kept under the fractional reserve requirements for the bank. So the advantage is that they don't reduce the leverage in the system. This is why central banks liked that model slightly more from a scale standpoint, compared to the fully backed stablecoins.

- Stablecoins are not under fractional reserve. By contrast to the previous point, the stablecoin concept calls for a one-to-one relationship, with every $1 of stablecoin matched by a $1 value behind it.

- USDF policy view. USDF - a membership-based association of FDIC-insured banks - believes that it’s critical for tokenised deposits to maintain a niche apart from stablecoins as legislation and regulation move forward.

- BIS View. On April 11th, the Bank for International Settlements (BIS) published a paper comparing stablecoins to tokenized bank deposits. In it, it argues that tokenized deposits are superior to stablecoins and that Tokenised Deposits support the ‘singleness’ of money.

- Join the roundtable “Who will Emerge the Digital Money Winner: Stablecoins or Tokenised Deposits?” on June 26th at Point Zero Forum.

- To learn more about digital assets, Elevandi offers a dedicated online course.

An Intro to Tokenised Deposits

Tokenised deposits are a type of financial asset that represent traditional bank deposits, such as savings or checking accounts, that have been converted into digital tokens. These tokens are typically created on a blockchain, which allows for the easy transfer of ownership and the tracking of transactions in a secure and transparent manner.

Tokenised deposits are designed to provide a number of benefits, including:

- Increased liquidity: By converting bank deposits into digital tokens, tokenised deposits can be easily and efficiently transferred, providing investors with greater liquidity than traditional bank deposits.

- Lower transaction costs: Since tokenised deposits are traded on a blockchain, transaction costs can be significantly lower than traditional banking fees.

- Increased accessibility: Tokenised deposits can be traded globally, making them accessible to a wider range of investors than traditional bank deposits.

- Programmability: Tokenised deposits can be programmed with smart contracts, which can automate a range of functions such as interest payments, collateralisation, and loan origination.

Transparency: Since tokenised deposits are created on a blockchain, transactions can be tracked in real-time, providing greater transparency and security than traditional banking.

An Intro to Stablecoins, Tokenised Deposits' competitors

Stablecoins are a type of cryptocurrency that aims to maintain a stable value relative to a particular asset, such as a fiat currency like the US dollar or a commodity like gold. They are designed to provide the benefits of cryptocurrencies, such as decentralisation and fast transaction speeds while minimising the volatility that is often associated with other cryptocurrencies like Bitcoin.

With the notable exception of algorithmic stablecoins like the defunct UST, stablecoins have become increasingly popular in recent years due to their stability and predictability. They are often used as a means of payment or a store of value, particularly in situations where traditional fiat currencies or cryptocurrencies may be too volatile or unreliable (Latin America, Africa).

Not all stablecoins are created the same way though. One group, including Tether and USD Coin (USDC), is built on the idea that a stablecoin is backed dollar for dollar by a basket of financial assets. You deposit one US dollar with Circle, and one USDC is minted.

Additionally, there are different models of stablecoins which include MakerDao’s DAI, Frax, Aave’s GOH, Curve’s crvUSD, RAI, and many more.

The less risky group is definitely the first.

How are tokenised deposits different? A deeper dive

Tokenised Deposits can be considered an evolution of, or an alternative to, the stablecoin concept.

Tokenised deposits are a reference to an existing bank deposit that is held as a liability against an insured depository institution.

Tokenised deposits are not designed to be purchased at exchanges, but function as an infrastructure layer to make bank payments more efficient.

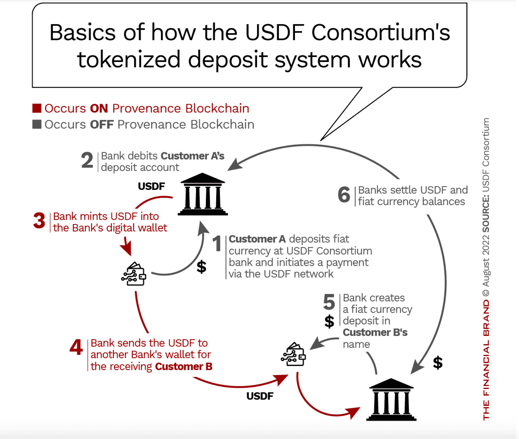

Let’s look at USDF as an example:

USDF is a bank-minted tokenised deposit referencing fiat currency on Blockchain. The USDF Consortium is a membership-based association of FDIC-insured banks.

Their mission is to build a network of banks to further the adoption and interoperability of a bank-minted tokenized deposit (USDF).

Here’s how it works:

An ongoing concern for banks in this area, and a key one for USDF, is the role of fractional reserves. A classic function of commercial banking intermediation of deposits is the creation of new money through lending. Lending creates new deposits which, subject to capital rules, can create more lending. Fractional reserve banking, as it is called, can drive economic growth, and banks have been doing this for hundreds of years.

By contrast, the stablecoin concept calls for a one-to-one relationship, with every $1 of stablecoin matched by a $1 value behind it.

Banks have been concerned about this idea in this context as well as in the development of central bank digital currencies, especially if issued directly by the Federal Reserve.

In its comments to Treasury, USDF makes a key argument: “Tokenised deposits … are the digital representation of existing liabilities — demand deposit claims — that a bank has on its balance sheet. Importantly, tokenized deposits are obligations of banks…”

USDF, therefore, believes that it’s critical for tokenised deposits to maintain a niche apart from stablecoins as legislation and regulation move forward.

“It’s important to maintain that separation because if you’re requiring full reserving, you’re forgetting the intermediation function banks serve and the credit creation function they provide.”

BIS’ View on Tokenised Deposits

On April 11th, the Bank for International Settlements (BIS) published a paper comparing stablecoins to tokenised bank deposits. In the document, it asserts that stablecoins are similar to the (unstable) era of privately issued bank notes before the creation of the U.S. Federal Reserve.

As evidence, it points to the de-pegging of the Tether stablecoin in the aftermath of the collapse of the FTX crypto exchange and a similar impact on Circle’s USDC when Silicon Valley Bank was shuttered, holding a smallish part of the USDC reserves.

In contrast, the BIS argues that tokenised deposits support the ‘singleness’ of money. In other words, that currency is interchangeable no matter the form.

The paper puts forward one specific model for tokenized deposits, but there are others.

The Oliver Wyman report on Tokenised Deposits

The report asserts that Tokenised Deposits would enable peer-to-peer settlements and make depository institutions’ money programmable and usable in smart contracts and other blockchain applications.

Despite the novel technology, in legal and economic terms, an on-chain tokenised bank deposit would be identical to a traditional off-chain deposit.

“We already have an efficient form of digital money; we just need to adapt it to a new environment. Central bank actions over the last century have resulted in a well-functioning banking and payment system. Why not take advantage of that, and issue tokenised deposits?”

For a deep dive, read the full report.

Point Zero Forum Roundtable on Tokenised Deposits

Point Zero Forum is a not-for-profit initiative of Elevandi, a spin-off of the central bank of Singapore (MAS), and the Swiss State Secretariat for International Finance. The aim is to promote a global policy and technology dialogue in Financial Services.

In this context, a series of leadership dialogues, public-private roundtables, and deep dive workshops are organised. One, in particular, covers Tokenised Deposits. Details are below.

Who will Emerge the Digital Money Winner: Stablecoins or Tokenised Deposits?

Monday, 26 June 2023, 2pm – 4pm

Roundtable Room, The Circle Convention Centre

Roundtable Objective: Stablecoins have long been recognised as a key enabler of the digital asset ecosystem, serving as a bridge between the fiat and tokenised realms. As a form of digital money, stablecoins boast functionalities that could support wider utility as a mode of payments for real world applications and usage. But recent developments have called into question the supposed stability of stablecoins and its reliability as a trusted medium of exchange. In tandem, there has been growing clamour advocating for tokenised deposits as the future of payments, bringing similar functionalities with purportedly less risk – but how much truth does this hold? Can they coexist, or is one destined to displace the other?

Featuring regulators and industry experts, this roundtable aims to deep dive into this debate – the merits and limitations of both fiat-backed stablecoins and tokenised deposits, insights into key drivers and contributing factors to success or failure; and how developing global regulations tie everything together.

Speakers:

1. Umar Farooq, CEO, Onyx by JP Morgan

2. Rene Michau, Global Head, Digital Assets, SCB

3. Nicolas de Skowronski, Head of Wealth Management Solutions, and Member of the Executive Boards, Bank Julius Baer & Co. Ltd.

4. Dante Disparte, Chief Strategy Officer, Head of Global Policy, Circle

5. Richmond Teo, CEO Asia, Paxos 6. Kathy Kraninger, Vice President of Regulatory Affairs, Solidus Labs

7. Adrian Ang, Allen & Gledhill

Discussants:

1. Ken Nagatsuka, Executive Director, Payments Department, MAS

2. Ryosuke Ushida, Chief FinTech Officer, Financial Services Agency of Japan

3. Adeline Bachellerie, Head of Digital Currency and Innovation, Banque de France

4. Thammarak Moenjak, Senior Advisor, Digital Currency Team, Bank of Thailand

5. Nicolas Brügger, Deputy Head of Capital Markets & Infrastructures, State Secretariat for International Finance (SIF)

6. John O’Neill, Managing Director, Global Head of Digital Asset Strategy, HSBC

7. Emma Butterworth, Head of Financial Market Infrastructure Innovation and Payments Policy Division, Bank of England

8. Oliver Buschan, Member of the Executive Board, Swiss Bankers Association

9. Tom Duff Gordon, Vice President International Policy, Coinbase

About the Author

Based in Asia, I’m an Italian author, investor, and passionate advocate of the blockchain revolution since my first venture in the space in 2015. I currently hold the positions of Business Development Head at Elevandi and GBBC’s Ambassador for Southeast Asia.

For more on AI, DeFi, NFTs, and Web3 subscribe to my Newsletter here.

COMMENTS